A critical illness policy is a policy that pays a tax-free benefit if you were to ever contract a critical illness and survive. The big 3 are heart attack, cancer and stroke…but in all, 25 different illnesses are covered in most critical illness policies. Just like life insurance, you can decide whether you want a policy that the premiums are guaranteed and locked in for 10 years, 20 years, to age 75 or to age 100. Also just like life insurance, you can decide the benefit amount of the policy that would pay out to you once diagnosed with one of these illnesses.

You can choose to add on a return of premium upon death benefit. What this means, is that if you were to pass away without ever collecting on your critical illness benefit, 100% of your premiums paid would be refunded to your beneficiary.

The second additional benefit that you can tack onto the critical illness policy is a return of premium benefit. What this means, is that after a certain amount of time of keeping the policy in place…you can cancel the policy and have all of your premiums refunded back to you. So basically the critical illness policy turns into a glorified savings account…where you will either get all your money back after canceling the policy (or death)…or the critical illness benefit will pay out tax-free.

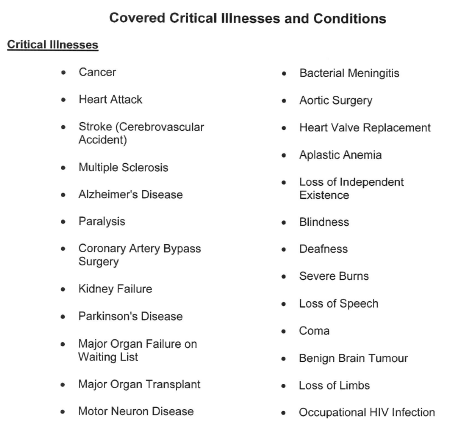

The list of covered conditions include…

So you need to ask yourself…how prepared am I if one of these illnesses were to occur. We may not realize that our provincial health care plan may not pay for all of the prescribed medication or treatments. What about the time away from work while you are recovering? Do you plan on using all of your savings to get you through this time period?…Do you even have enough savings to do so? This is where even a $50,000 or $100,000 policy might be the perfect fit. And the best thing is once the tax-free cheque is delivered, it’s your decision on how best to spend it. Do you want to skip the line and get treatment down in the States? Would you like to take extra time off of work to recover? Are there going to be bills that you never even imagined…like wheelchair accessibility, or even to help to financially allow a loved one to take time off work to help take care of you. I know it’s hard to picture it could happen to your scenario…but unfortunately, we are starting to become the reality that you can just ask your neighbor how it affected them.